I predict that 2016 will be the year of contactless payments. Apple Pay, Android Pay and Samsung Pay will continue to grow in adoption. This is largely due to the fact that here in the US most merchants must upgrade their point of sale terminals to accept “chip (EMV)” based credit cards. While they are in the process of doing that, those new terminals will also be able to accept NFC Contactless Payments. That’s GREAT! What about the little guy? The mom and pop shops that don’t have a brick and mortar location. The dog walker, baby sitter, fitness trainer, bake sale, users group, mechanic, lawn service, photographer, housekeeper, consultant, tutor, makeup artist, hair stylist, yard sale, etc. can now join in on this revolution thanks to…

It seems like there are very few situations where “we can all just get along”. When Apple introduced Apple Pay and support for the over 220,000 merchants already taking NFC wireless payments at the register, I thought “sweet!” Everyone loves a faster checkout experience and having one that’s more secure and private can only be a good thing right? Although CVS was never listed as one of the vendors to support Apple Pay, there were people reporting that it was working at their local CVS stores. This is because CVS has/had NFC wireless payments already in place for Google Wallet and other forms of wireless payments. Soon after these reports started coming in, we started to see reports that CVS purposely disabled not only Apple Pay, but NFC payments period! Yes, even Google Wallet on Android, which was already working and in place before Apple Pay.

Why would CVS, Rite Aid and others purposely block Apple Pay and NFC payments?

Well the answer seems to be they are throwing their weight behind a different mobile payment system called CurrentC. CurrentC isn’t live yet and isn’t slated to go live until early 2015. Hmm, ok. So your new payment system isn’t ready yet, then why disable one that is ready and already working at your registers? The answer to that seems to be an “exclusive” deal with CurrentC that states in writing that these merchants aren’t allowed to accept payments from competing systems. Hmmm, ok. Then why shut if off now. My guess is that they wanted to cut off support for Apple Pay before users got used to using it at their stores. In other words if something never worked you’d be less likely to complain (too loudly) than if something worked for months and then stopped working. Again, this is my personal guess, but it makes sense. It could also just be a coincidence in timing, but it seems to convenient to be a timing thing. The only other question I would have is why would you sign a deal that blocked your customers from using other payment methods especially if you already had the necessary hardware in place? As usual, it’s always about money. In other words, if CurrentC offered a better deal with less fees then the merchants just did the math and went with the better deal. What about the customer you ask? Well that’s the point of this post. At the end of the day customers always decide with their wallet what will succeed and what won’t

The NFC capable terminal at Whole Foods Market

Can’t we just use CurrentC AND Apple Pay/Google Wallet?

The first thing that a consumer might think is “why not use both?” There’s certainly nothing stopping you from using both Apple Pay/Google Wallet AND CurrentC. It’s not like your smartphone is only capable of one payment system. Since CurrentC will use a dedicated App for both iOS and Android it’s easy for consumers to use both. As a matter of fact more iPhone users will be able to use it than Apple Pay because it doesn’t require NFC hardware to be in your iPhone. However, everything I’ve read thus far promises that CurrentC will be a disaster for the consumer. Here’s why: first off it’s linked to your checking account, not your credit and debit cards. This is probably why merchants are attracted to this payment system because it will reduce the credit card fees that they pay. This probably isn’t the end of the world for many at places like RiteAid and CVS, but BestBuy is on the list to get this too and I don’t know of too many people that buy big ticket items using the money in their checking accounts. People typically pay for these items over time. Next, the signup requires not only your banking information, but also your Social Security Number and your Driver’s License Number. If that’s not enough to stop you in your tracks right there, it almost promises to be slower at checkout time due to the back and forth QR code scanning that not only you have to do, but the clerk has to do as well. The clerk rings up your purchase and you then scan the QR code that’s on the display with your phone using the CurrentC app. Nope you’re not done. You then show the clerk the QR code that the app produced on your phone so that he/she can scan it as well. What could go wrong?

The Bottom Line – I have a choice

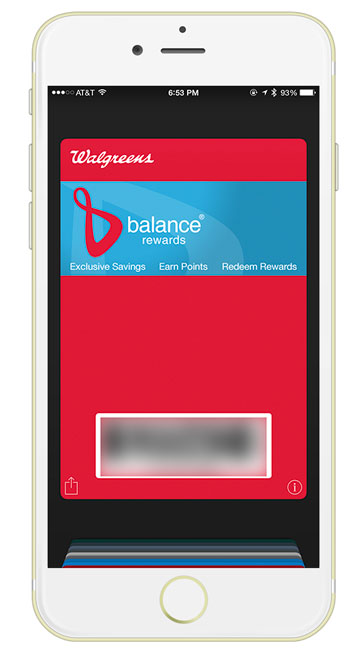

By the way CVS, see the nice location based Walgreens Rewards Card in Passbook? You’ve promising this feature for over a year. Just sayin’

The funny thing is that I actually preferred going to CVS simply because it was closer to where I lived than either Walgreens or RiteAid. Proximity to my home made CVS my default choice. Now that’s no longer the case. Where I live now, the nearest CVS is directly across the street from a Walgreens. When I pull up to the intersection I can make a left and go into the Walgreens parking lot or make a right and go into the CVS parking lot. Since Walgreens makes it easier, faster and more secure to do my checkout in their stores with Apple Pay, it looks like I’ll be buying more from Walgreens from here on out. This is what I mean by “customers decide what succeeds and what doesn’t with their wallets.” I very rarely try to predict the future, but when it comes to CVS vs Walgreens (CurrentC vs ApplePay/Google Wallet)? Walgreens just gained at least one new customer. CurrentC is a non-starter for me. Making it harder to take your customer’s money usually doesn’t workout to well for the merchant. Lastly this just in… “In 72 hours, Apple Pay is already the wireless payment leader in the US”

Sadly it seems pretty common place these days to hear of big companies being hacked and having thousands, if not millions of credit card numbers stolen and resold. When Apple announced Apple Pay, I was very interested to say the least. The idea of a payment system that breaks away from all the traditional pitfalls of credit/debit card payments is something that we can all appreciate. The concept behind Apple Pay is simple. If you have an iPhone 6 or iPhone 6 Plus then you have the necessary hardware (NFC – near field communications) to allow for wireless transmission of data from your phone to a payment terminal at the cash register. However, instead of sending your credit card number, name, phone number, email address and card ID, a token is sent instead. The token itself is USELESS to hackers. Therefore if the merchant is hacked they never had your credit card number or information about you to lose. Sign me up!

Setting up Apple Pay

This past Monday iOS 8.1 was released which allowed for Apple Pay to be setup on the iPhone 6 and iPhone 6 Plus. The setup process is very easy. Apple Pay is now a part of Passbook on your iPhone. First off if you have a credit/debit card on file with your Apple ID, you can immediately add it. All you’ll need is the card ID from the back for verification. You can then proceed to add additional cards by simply hitting the + sign and either using the built-in camera to OCR the card info or you can key it in manually. The camera worked for all but one of my cards. I was able to easily add four additional cards. The only one that gave me trouble was a Chase Slate credit card. While the card was easily added, I had to call them to actually activate it for Apple Pay. The number displayed during the setup process and I was able to tap and call it right from the Apple Pay area of Passbook. It took three calls as I was disconnected twice to get through the process. Actually I ended up deleting that card and re-adding it and it was then approved immediately.

Using Apple Pay with other Apps on your iPhone

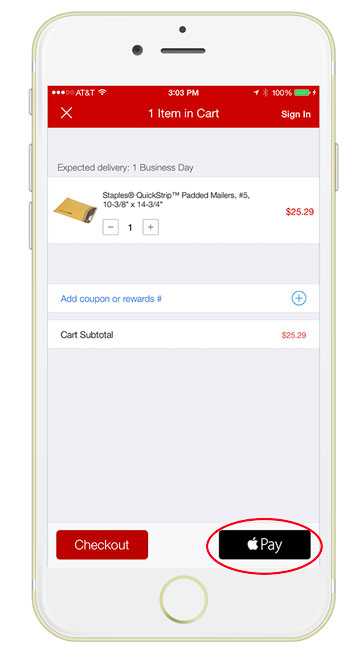

Although I could have gotten in my car and headed out to one of the merchants that supports Apple Pay, I decided to test it first right from my office chair by placing an online order. Several apps got updated on Monday including Staples, Target, Uber, Apple Store, Hotel Tonight, Groupon, Open Table and others. Since there was an office supply item I needed I decided to order it with the Staples app and pay with Apple Pay. I fired up the Staples app and searched for the the item I wanted. I added it to my cart and tapped check out. Once I got to the checkout screen I had the option of either signing in to my Staples account, checking out as a guest or tapping the Apple Pay button. Once I tapped the Apple Pay button I was able to then choose which card I wanted to use, which address I wanted to ship my order to and which phone number and email address I wanted to use for shipping the order. I later found that in the Apple Pay settings in iOS 8.1 you can set all the defaults you want to use. I tapped pay and put my finger on the finger print scanner and that was it. My order was placed. I didn’t have to key anything in. It was awesome as online ordering on a phone can be a pain in the butt.

Using Apple Pay at a retail location.

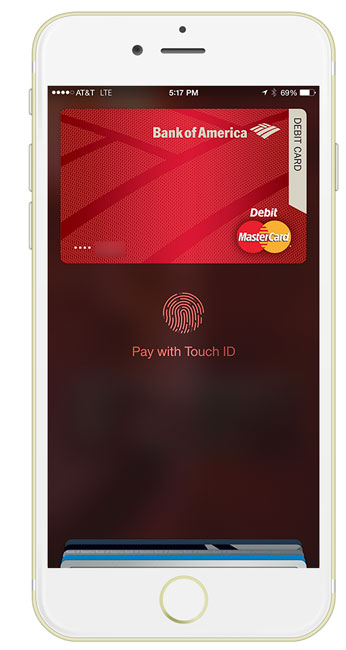

Yesterday I decided to give Apple Pay a try at my local Walgreens. It was the closest store to me that accepts Apple Pay besides McDonalds. While the process was relatively quick, it wasn’t as “touchless” as I imagined. The first thing that I learned from the Staples experience above is that by not signing in, I didn’t get any Staples Rewards. Well the same thing applies at the register. You will still need to present your store loyalty card if you want points/discounts. Luckily my Walgreens card is also in Passbook. I handed the clerk my iPhone so that she could scan the barcode on my Walgreens card first. Then she rang up my two items. Once she was done I put my iPhone up to the sensor to start the Apple Pay process. My default debit card appeared on the screen and I used my finger to approve the transaction. AWESOME! Done right? Well not yet. Once I saw the “Approved” appear on my iPhone I put my iPhone away, but I still had to tap Credit vs. Debit AND approve the amount on the terminal. I assume that had I used a credit card vs. a debit card then I would have probably bypassed that first question. However, it was still odd that I had to tap that I approve the amount after the fact. Nonetheless, she handed me my receipt and I was out the door.

A short video of my first Apple Pay at a retail location:

The Bottom Line

Apple Pay will definitely move us one major step closer to replacing the traditional wallet. Instead of physically carrying 3, 4 or 5 cards now I may only carry one or two because the others are in Apple Pay if I want to use them. It was also a good feeling knowing that Walgreens didn’t just get my debit card number and If I wanted to be totally anonymous then I could have not given my rewards card. If you have an iPhone 6 or iPhone 6 Plus I can’t think of any reason not to use Apple Pay. It’s certainly much more secure than handing over your physical card. Apple Pay can’t be used by someone else even if they steal your phone because of the required finger “touch-ID”. You can also remotely wipe all your information including pay information from a lost or stolen iPhone via the Find My iPhone feature. Apple also has the clout to bring over most of all the major players, so they are likely to succeed where others have failed at this.

As of today you can use Apple Pay with the following Bank Cards (AMEX, Visa and Mastercard) from: American Express, Bank of America, Capital One, Chase, Citi and Wells Fargo with more banks coming this year like barclaycard, Navy Federal Credit Union, PNC, USAA and US Bank. Apple says that you can use Apple Pay at 220,000 stores and counting, including: Aeropostale, American Eagle Outfitters, Apple Stores, BabiesRus, BJs, Bloomingdales, Champs, Chevron, Disney Store, DuaneReade, ExtraMile, Foot Locker, FootAction, Macy’s, McDonalds, Meijer, Nike, Office Depot, Panera Bread, Petco, Radioshack, Six:02, Sports Authority, Subway, Texico, ToysRus, Unleashed, Walgreens, Whole Foods or anywhere else you see this icon:

Some are reporting Apple Pay working at stores others than the ones Apple lists, so give it a shot if you see the wireless pay icon above. See Apple’s list here.